Which factors make up my credit score?

Your credit score is made up of several factors and understanding the impact of each will help you maintain a good score.

What is a credit score?

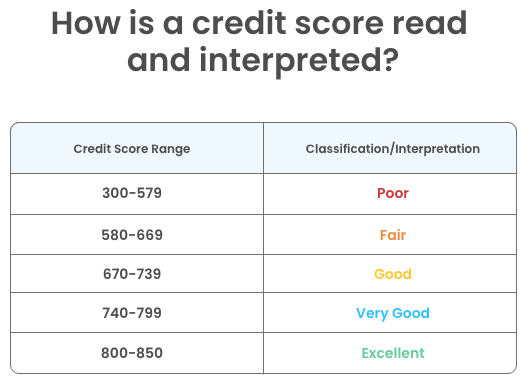

A credit score is a three-digit number that indicates to banks and other lenders how likely you are to pay back the money you borrowed. Based on this, they decide whether to give you a loan/credit card or not and at what rate of interest/credit limit, respectively. In other words, they use this score to determine whether you are ‘worthy of credit’ or not. Hence, in financial terms, we say the credit score represents the ‘credit worthiness’ of a customer.

Note: The above figures can vary slightly based on each credit bureau

Where can I check my credit score?

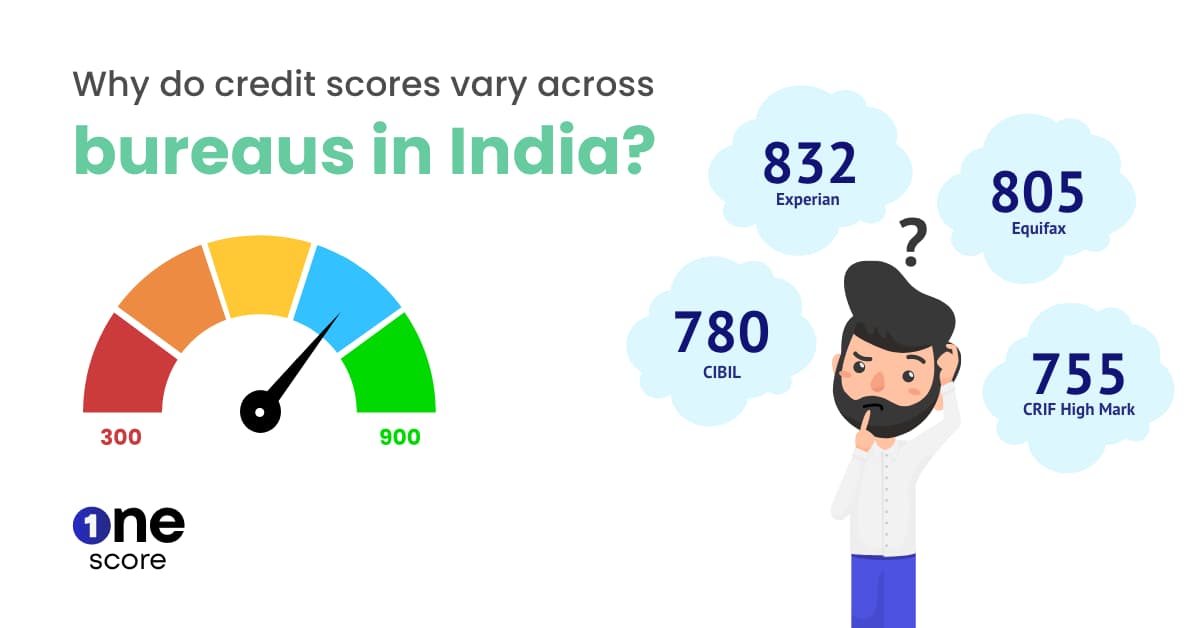

There are four credit scoring agencies, also called credit bureaus, that give you credit scores - TransUnion CIBIL, Experian, Equifax, and CRIF High Mark. Each credit bureau uses its own set of formulas and algorithms to calculate the score for every individual. Hence, each bureau’s credit score differs from the other.

You can get each score by contacting these bureaus, but a quicker and easier way to do it is to download the OneScore app and get your CIBIL & Experian score in less than 3 mins.

What do I do if I don’t have a score?

You should start building your credit score immediately as it increases your chances of getting a loan and/or credit cards in the future. The fastest and easiest way to start building your credit score from zero, is by creating an FD and getting a One Credit Card. It is the only FD backed card that gives you a credit limit of 110% of your FD amount. Additionally, you earn interest on your FD @ 6.1% p.a. Click on the link here to get your FD backed One Credit Card!

What are the factors affecting my credit score?

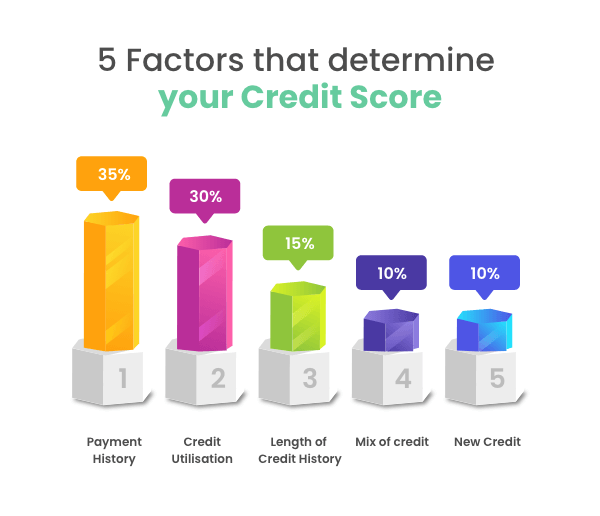

There are five factors that affect your credit score -

1) Payment History

The most important factor while calculating your credit score is payment history. Any missed payment, be it big or small, impacts your credit score negatively. Not only does your score drop, but lenders also take it as a sign of a possible default behaviour from you in the future. So maintain a good score, ensure you make timely payments on your loans and credit cards.

2) Credit Utilisation

Credit utilisation stands for the total amount of your credit limit (all credit cards put together) which you have spent in a month, divided by the combined credit limit you have on all your cards.

For e.g., If you have a total credit limit of Rs 1,00,000 and used Rs 50,000 of your credit limit. Then, your credit utilisation will be 50%. If you are overusing your credit limit, lenders think of you as someone who spends more money than they can manage. Hence, try not to use your entire credit limit.

3) Length of Credit History

While calculating your credit score, bureaus don’t consider your age, but they do consider how many years it has been since the first time you took a loan or a credit card and when you took your newest loan or credit card. They also consider the average age of all your credit accounts (loans + cards) combined. The older the age of your first credit account, the better it is.

4) Mix of Credit

Mix of credit refers to the type of accounts that show up on your credit report. There are two types of credit accounts - instalment based (loans) and revolving (credit cards). A mix of both these types of credit accounts shows the lender your ability to manage various kinds of credit products and hence are a good customer to lend to.

5) New Credit

The number of new credit accounts you have opened in the recent past, along with the credit products you have applied for currently, make up your new credit.

Every time you apply for a new loan or credit card, the lender will make a hard inquiry. A hard inquiry is one where the lenders pull your credit report from the bureaus to check your credit score and hence creditworthiness. Unlike a soft inquiry (where you pull your score yourself) which doesn’t affect your credit score, too many hard inquiries in a short time frame can negatively impact your credit score.

To conclude, lenders use your credit score to decide whether to give you loans and credit cards in the future. So, it is essential to keep your credit score above the range of 700 at all times. If your score is low, don’t delay any more! Download the OneScore app, use the score improvement planner and get a FD backed One Credit Card and start improving your score by just using it. Take a step towards a happy and healthy financial life!

**Disclaimer: The information provided on this webpage does not, and is not intended to, constitute any kind of advice; instead, all the information available here is for general informational purposes only. FPL Consumer Services Private Limited and the author shall not be responsible for any direct/indirect/damages/loss incurred by the reader in making any decision based on the contents and information. Please consult your advisor before making any decision.

- OneScore , July 13, 2021